Car insurance premiums can vary widely depending on several factors. Understanding what affects your insurance premium is crucial to making informed decisions and finding ways to save on your monthly payments. From your driving record to the type of vehicle you drive, many elements play a role in determining how much you’ll pay for car insurance. In this blog, we’ll explore the key factors that influence your auto insurance rates and provide tips on how you can lower them.

Your Driving History

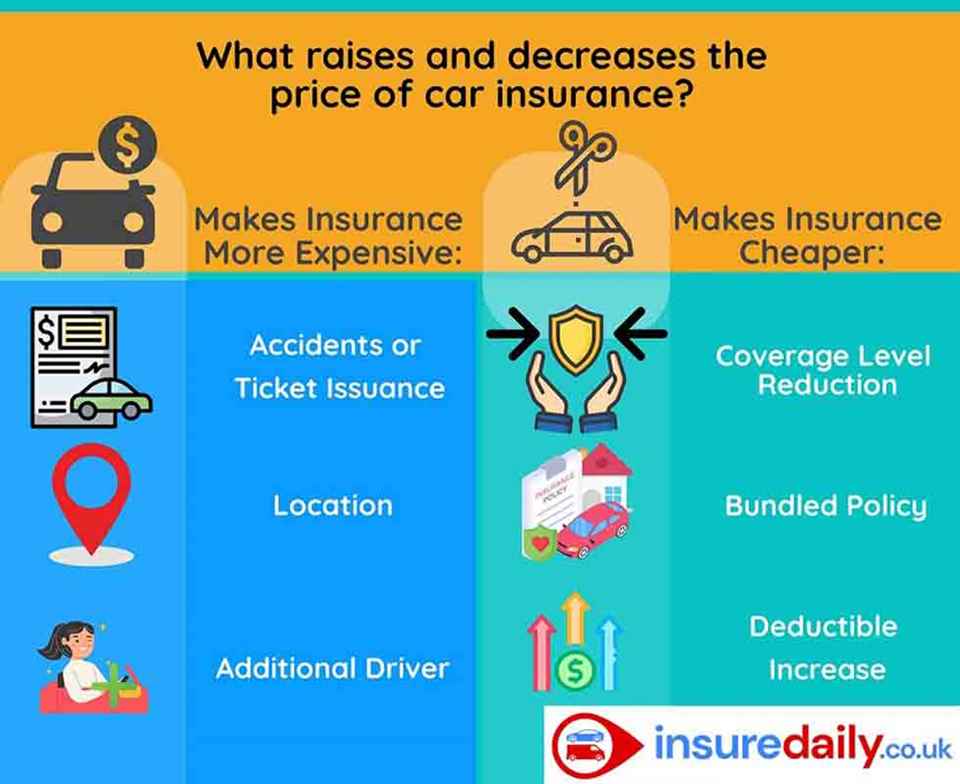

One of the most significant factors affecting your insurance premium is your driving record. Insurers assess your history to determine how likely you are to be involved in an accident or file a claim. If you have a clean driving record, you are seen as a lower risk and are likely to pay less for insurance. On the other hand, if you have a history of traffic violations or accidents, your rates may increase.

Traffic Violations: Speeding tickets, running red lights, or any other moving violations can raise your premiums. Serious violations like DUI or reckless driving can lead to even higher increases.

Accidents: If you’ve been involved in an accident, especially one where you were at fault, your insurance premiums are likely to increase. Multiple accidents may lead to higher premiums over time.

How to Lower Your Premium: Maintaining a clean driving record is the best way to keep your premiums low. Consider taking a defensive driving course to reduce points on your record and demonstrate your commitment to safe driving.

Your Vehicle

The type of vehicle you drive can have a significant impact on your insurance costs. Insurers evaluate several aspects of your car when determining your premium:

Make and Model: Luxury vehicles, sports cars, and high-performance cars are more expensive to insure due to the higher costs of repair or replacement. On the other hand, family cars and sedans generally cost less to insure.

Safety Features: Cars equipped with advanced safety features, such as automatic braking, lane-keeping assistance, airbags, and anti-theft systems, can lower your premiums. These features reduce the risk of accidents and theft, making you a lower risk for insurers.

Vehicle Age: New cars typically cost more to insure, while older vehicles may have lower premiums because their value is less. However, older cars may not have modern safety features, which can sometimes offset the lower cost.

How to Lower Your Premium: If you’re in the market for a new car, consider choosing a model that is affordable to insure. Additionally, installing safety features or anti-theft devices may help reduce your premium.

Your Location

Where you live plays a role in your car insurance premium. If you live in an area with high traffic volume, crime rates, or a history of natural disasters, your insurance rates are likely to be higher.

Urban vs. Rural Areas: Drivers in cities with heavy traffic and higher accident rates tend to pay more for insurance. In contrast, drivers in rural areas with less traffic might have lower premiums.

Crime Rates: If you live in an area known for car theft or vandalism, your premiums may be higher to account for the increased risk of damage or loss.

Weather and Natural Disasters: Areas prone to extreme weather (like hailstorms or floods) or natural disasters (like hurricanes or earthquakes) may also result in higher premiums, as your car is at greater risk of being damaged.

How to Lower Your Premium: If you live in a high-risk area, consider moving your car to a secure garage or using anti-theft devices to lower your risk. Additionally, check with your insurer to see if they offer coverage for specific weather-related risks.

Your Credit Score

In many states, including Texas, your credit score can affect your car insurance premium. Insurers believe that individuals with higher credit scores are less likely to file claims, making them a lower risk.

Better Credit = Lower Premiums: If you have a good credit score, you may qualify for lower rates. On the other hand, individuals with poor credit scores may pay higher premiums.

How to Lower Your Premium: Maintaining a strong credit score can help reduce your insurance costs. Pay bills on time, reduce debt, and regularly check your credit score for errors.

The Amount of Coverage You Choose

The amount and type of coverage you select will also directly impact your premium. The more extensive the coverage, the higher your premium will be. Here are the main types of coverage to consider:

Liability Insurance: Covers the other party’s expenses if you’re at fault in an accident. It’s required by law, but you can choose higher or lower limits based on your needs.

Collision Coverage: Covers damage to your own vehicle, even if you’re at fault. It’s optional unless required by your lender if you’re financing or leasing your car.

Comprehensive Coverage: Covers damage to your car caused by events other than a collision, such as theft, vandalism, or weather-related damage. It’s optional but may be required for financed vehicles.

How to Lower Your Premium: While adequate coverage is important, you can reduce your premium by adjusting your coverage levels. However, be careful not to skimp on coverage to save a few dollars, as you may end up paying more in the event of a claim.

Your Age, Gender, and Driving Experience

Age, gender, and the amount of experience you have behind the wheel also influence your premiums. Here’s how:

Young Drivers: Drivers under 25, especially teens, tend to have higher premiums due to their lack of experience and higher risk of accidents.

Older Drivers: Older, more experienced drivers usually enjoy lower premiums, though rates may rise again once drivers reach their 60s or 70s.

Gender: Statistically, young male drivers are more likely to be involved in accidents, leading to higher premiums. However, the gap often narrows as drivers get older.

How to Lower Your Premium: Young drivers can reduce premiums by taking a driver education course or maintaining a clean driving record. Older drivers may qualify for discounts as they age and gain more experience.

Your Insurance Provider

Different insurance companies have different pricing models and offer varying discounts. Shopping around and comparing rates from different insurers can help you find the best deal for your needs.

Discounts: Many insurers offer discounts for things like bundling policies, driving fewer miles, maintaining a good driving record, or installing anti-theft devices in your car.

Customer Service: Consider the reputation of the insurance provider when choosing a company. Good customer service can make a big difference when you need to file a claim.

How to Lower Your Premium: Get quotes from multiple insurance providers to compare rates. Don’t be afraid to ask about available discounts and look for companies with a strong reputation for customer service.

Understanding what affects your car insurance premium is key to making smarter decisions that can save you money. By considering factors like your driving history, the vehicle you drive, and the amount of coverage you select, you can better control your rates. Shop around for the best deals, maintain a clean driving record, and take advantage of discounts to keep your premiums as low as possible.

Stay proactive, review your insurance options regularly, and ensure you’re getting the best value for your car insurance needs.